Rocket Society Financing firmly believes for making data-motivated expenditures that are informed by the groups i serve. That’s why i created our very own flagship community engagement program, Neighbor to help you Neighbor, hence happens door-to-door hooking up customers so you’re able to critical tips whilst get together investigation in order to posting future investments. In the event Next-door neighbor to Neighbors began within the Detroit with a focus on income tax foreclosures avoidance and you can change, you will find once the extended the application form in order to Cleveland and you can, in the 2023, in order to Atlanta.

How do you Improve your Odds of Being qualified Getting Home financing Which have Student loan Debt?

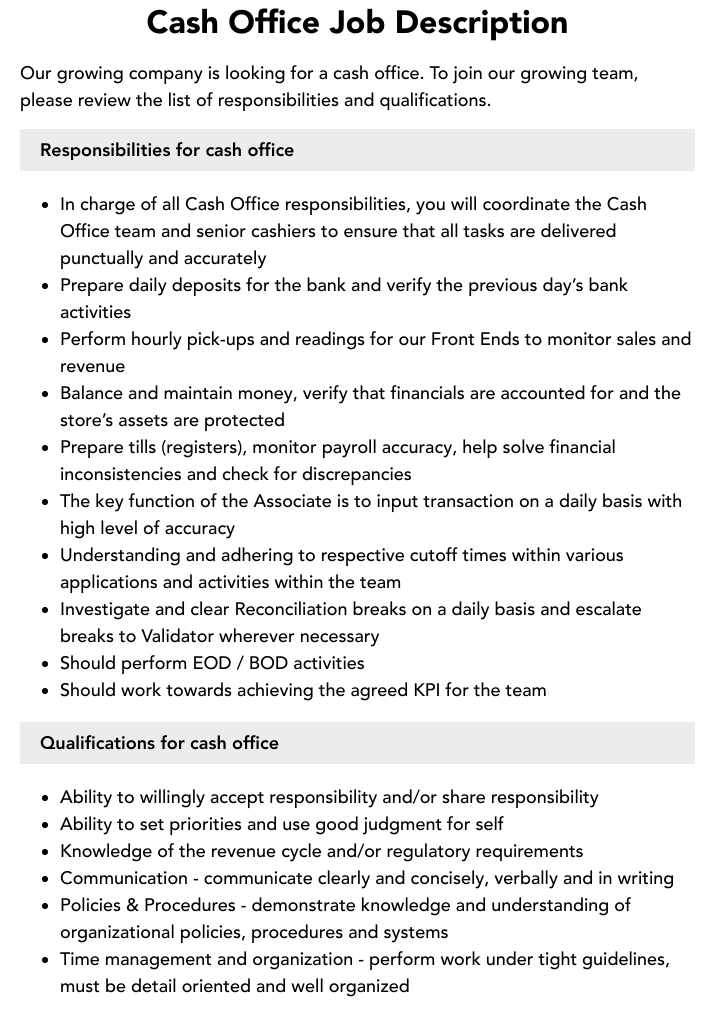

Illustration of DTI

Let us mention a typical example of exactly how DTI work for the real-world. In this example, you’ve got an entire disgusting monthly money away from $5,one hundred thousand. As well as your monthly expenses is actually below:

Earliest, why don’t we add up your monthly costs. In cases like this, the overall monthly bills create total $step 1,five-hundred. Second, we’re going to divide the brand new $1,five-hundred from the $5,000. So, your own DTI ratio try 0.30, otherwise 31%.

Just take a minute to incorporate up your DTI proportion observe exactly how your payments pile up against your revenue. In case the DTI is more than fifty%, that might be way too high in order to be eligible for a home loan. Whenever possible, run paying down expense to lessen the DTI proportion.

For those who have student loan financial obligation, that’ll not necessarily stand in just how off qualifying having an effective financial. But when you are concerned that the sized your scholar loan costs often limit your real estate ventures, below are a few an effective way to replace your mortgage acceptance possibility.

Imagine All types of Lenders Nowadays

Not all the financial sizes are built similarly. That is especially true regarding homeowners with student loan obligations. You should discuss any options to maximize your home loan approval odds.